No bushfire, storm or flood cover in the first 72 hours of your policy. Very limited exceptions apply. Actions or movements of the sea and storm surge are not covered (unless the storm surge damage occurs at the same time as damage caused by storm). Limits and exclusions apply.

GIO Insurance

We know insurance, so you know you’re covered.

Helping you take care of what matters

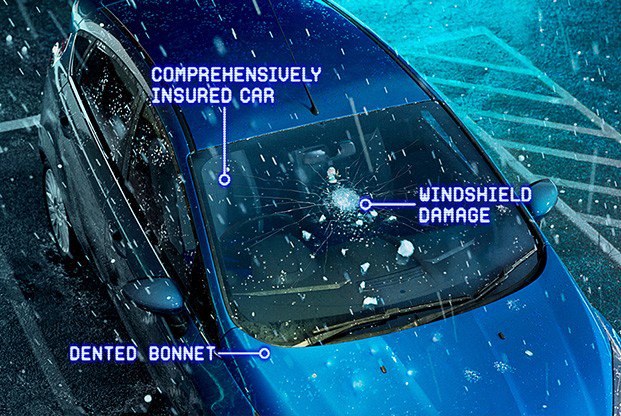

Car Insurance

Choose from a range of coverage options so you can find cover that suits your car, your needs and your budget.

CTP Insurance

Sort out your CTP so you can register your car with ease, and have cover for your liability for injuries caused to others in a motor vehicle accident.

Customise

Ways to save on Insurance

Ways to save

You shouldn't have to compromise on quality to save money. That's why we offer a range of ways to save on a GIO insurance policy, while maintaining the cover we know you deserve.

Multi-policy discount

Hold any 3 or more eligible policies with GIO and we’ll give you a multi-policy discount of 10%^. So if you’re a GIO customer, or thinking of becoming one, you can save on reliable coverage from a trusted insurer.

Online

Manage your insurance on the go

Benefits

Why Aussies might choose GIO

24/7 claims

(Excludes CTP and MAI)

Lodge your car or home insurance claim any time, online or over the phone. For CTP or MAI Insurance products, claims are only available on the phone during business hours.

Flexible cover

(Excludes CTP and MAI)

Choose the level of cover you need, adjust your excesses with eligible policies, and pay monthly or annually.

A trusted partner

Be confident with our innovative repair network and stress-free claims lodgement.

Ways to save

Eligible customers can enjoy discounts such as claims free savings on Comprehensive Car policies, and multi-policy discounts^.

News and info

Good to know about GIO

Showing of

Get in the know with GIO

Our Know More blog has articles and advice on a range of insurance-related topics.

Try and avoid damage with Hail Alerts

If your house is at risk of being hit with something like severe rain, hail or strong wind, we’ll let you know if you have registered and downloaded the GIO App. You can also manage your insurance policies, make and track claims, update personal details, renew policies, and more.

Why it’s important to have roadside assistance

On-call 24-hour assistance could be helpful for many of life’s issues. Explore how roadside assistance can help with your broken-down vehicle, leaving you with one less thing to deal with.

*No bushfire, storm or flood cover in the first 72 hours of your policy. Very limited exceptions apply. Actions or movements of the sea and storm surge are not covered (unless the storm surge damage occurs at the same time as damage caused by storm). Limits and exclusions apply.

^A multi-policy discount (MPD) rewards you with a discount off your premium for holding three or more eligible paid general insurance policies with GIO. Eligible policies that qualify for the MPD are: Home Building, Home Contents, Landlord Property, Landlord Contents, Car, Motorcycle, Caravan (including trailer) and Boat Insurance. Where applicable, an eligible policy includes any level of cover selected for that policy type. A GIO NSW CTP Green Slip and a GIO ACT MAI insurance policy count as eligible policies, but the premium for these policies cannot be discounted. Discount not applicable to Roadside Assist optional cover, CTP Green Slips, MAI Insurance policies, GIO Home Assist optional cover, Excess-free Glass optional cover or Domestic Workers Compensation optional cover. The discount is generally applied to the premium before we add taxes and charges. If you are eligible for more than one discount we usually apply any subsequent discount to the already discounted premium. See full Terms and Conditions.

Insurance issued by AAI Limited ABN 48 005 297 807 trading as GIO. Read the Product Disclosure Statement before buying this insurance. Target Market Determination is also available. This advice has been prepared without taking into account your particular objectives, financial situation or needs, so you should consider whether it is appropriate for you before acting on it.

Floods

No bushfire, storm or flood cover in the first 72 hours of your policy. Very limited exceptions apply. Actions or movements of the sea and storm surge are not covered (unless the storm surge damage occurs at the same time as damage caused by storm). Limits and exclusions apply.

Free Safety Net Home Protection

If you need to repair or rebuild your home after an insured event, you won't be limited by your sum insured - if the costs exceed that figure, we'll pay you up to 25% more. Offer ends 12/01/2023. Terms and Conditions apply.

Floods

No bushfire, storm or flood cover in the first 72 hours of your policy. Very limited exceptions apply. Actions or movements of the sea and storm surge are not covered (unless the storm surge damage occurs at the same time as damage caused by storm). Limits and exclusions apply.